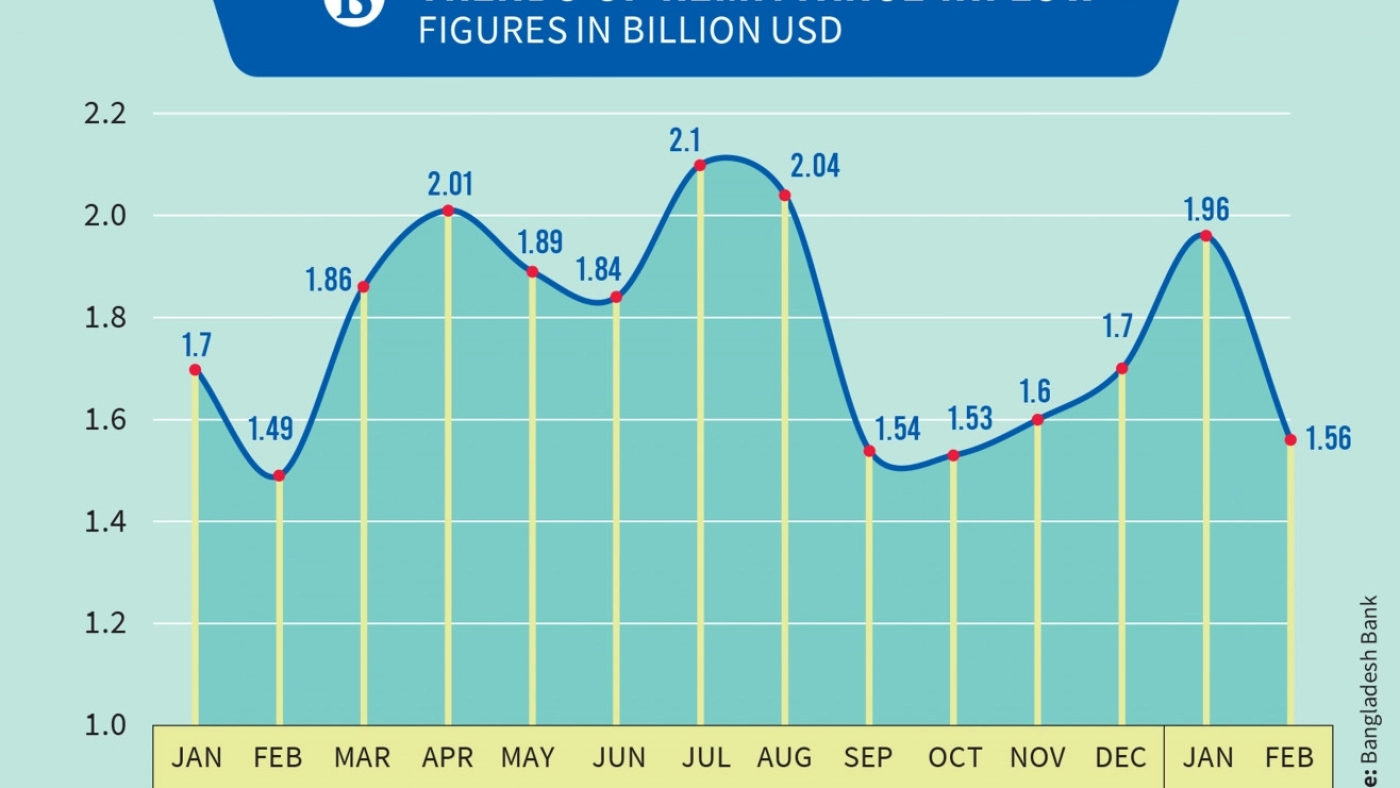

বিশ্ববাজারে দাম কম আর সরকারের কঠোর নিয়ন্ত্রণে কমেছে আমদানি। গত বছরের ফেব্রুয়ারির তুলনায় কমার হার ৩৯ শতাংশ।

ফেব্রুয়ারিতে সর্বনিম্ন আমদানি

করোনা কাটিয়ে বিশ্ব অর্থনীতি ঘুরে দাঁড়াতে শুরু করায় ২০২০ সালের শেষ দিক থেকেই পণ্যের দাম বাড়তে শুরু করে। ২০২১ সালের পুরো সময়টা ছিল পণ্যের দামে উত্থানের। ২০২২ সালে রাশিয়া–ইউক্রেন যুদ্ধ পণ্যের দাম আরও বাড়িয়ে দেয়।

যুদ্ধ শুরুর মাস অর্থাৎ গত বছরের ফেব্রয়ারি মাসে ১ কোটি ২৩ লাখ টন পণ্য আমদানিতে ব্যয় হয়েছিল ৮১৮ কোটি ডলার। আমদানি নিয়ন্ত্রণ করায় চলতি বছরের ফেব্রুয়ারি মাসে আমদানি ব্যয় কমে দাঁড়ায় ৫০৩ কোটি ডলারে। এ সময় আমদানি হয় এক কোটি চার লাখ টন পণ্য। অর্থাৎ ব্যয়ের হিসাবে কমেছে প্রায় ৩৯ শতাংশ। আর পরিমাণে কমেছে ১৫ শতাংশ।

জাতীয় রাজস্ব বোর্ডের (এনবিআর) তথ্যে দেখা যায়, আমদানি নিয়ন্ত্রণ ও বিশ্ববাজারে পণ্যের দাম কমতে থাকায় আমদানি ব্যয় কমতে শুরু করে নভেম্বর মাস থেকে। এরপর ধারাবাহিকভাবে গত ফেব্রুয়ারি পর্যন্ত আমদানি কমছে। গত নভেম্বর মাসে আমদানি ৭৭৩ কোটি ডলার থেকে ডিসেম্বরে নেমে আসে ৬৩২ কোটি ডলারে। আবার জানুয়ারিতে আমদানি ব্যয় ছিল ডিসেম্বরের কাছাকাছি অর্থাৎ ৬৩৫ কোটি ডলার। আর গত মাসে আমদানি ব্যয় সর্বনিম্ন পর্যায়ে পৌঁছায়।

এনবিআরের তথ্যানুযায়ী, চলতি ২০২২–২৩ অর্থবছরের আট মাসে (জুলাই–ফেব্রুয়ারি) পণ্য আমদানি হয়েছে ৫ হাজার ৩৮৩ কোটি ডলার। গত অর্থবছরের একই সময়ে ছিল ৫ হাজার ৭৩২ কোটি ডলার। অর্থাৎ ৩৪৯ কোটি ডলারের আমদানি ব্যয় কমেছে।

চট্টগ্রাম বন্দরের জেটিতে জাহাজসংখ্যার হিসাবে ধারণা করা যায়, পণ্য আমদানি কমার এই প্রবণতা থাকবে মার্চেও। মার্চ মাসের প্রথম তিন দিন চট্টগ্রাম বন্দরের জেটি অর্ধেকের বেশি ছিল ফাঁকা। জাহাজ না থাকায় জেটি খালি পড়ে ছিল। এই চিত্র অব্যাহত থাকলে মার্চেও আমদানি কমতে পারে।

আমদানি কমছে–বাড়ছে

আমদানি হ্রাস ও বৃদ্ধির তালিকায় অনেক পণ্য রয়েছে। বিলাস পণ্য আমদানি যেমন কমেছে, তেমনি শিল্পের আমদানিও কমে গেছে। যেমন বস্ত্রশিল্পের কাঁচামাল তুলার আমদানি কমেছে। চলতি অর্থবছরে আট মাসে ১০ লাখ ৯২ হাজার টন কাঁচা তুলা আমদানি হয়। গত অর্থবছরে একই সময় আমদানি হয়েছিল ১২ লাখ ৬৯ হাজার টন। পরিমাণে কমলেও আমদানি ব্যয় এখনো বেশি। চলতি অর্থবছরে আট মাসে তুলা আমদানিতে ব্যয় হয় ৩১২ কোটি ডলার। গত অর্থবছরে একই সময়ে ছিল ২৮৫ কোটি ডলার।

রড উৎপাদনের কাঁচামালের আমদানিও কমেছে। চলতি অর্থবছর এখন পর্যন্ত ১৩০ কোটি ডলারের পুরোনো লোহার টুকরা আমদানি হয়। গত বছরের একই সময়ে ছিল ১৫৬ কোটি ডলার। পুরোনো জাহাজ আমদানিও কমেছে। পুরোনো জাহাজ মূলত রড তৈরির কাঁচামালের দ্বিতীয় উৎস।

অর্থবছরের আট মাসে বিলাস পণ্য ফল আমদানি কমেছে। যেমন আপেল আমদানি ১ লাখ ৭৭ হাজার টন থেকে কমে দাঁড়িয়েছে ১ লাখ ২১ হাজার টনে। ভোগ্যপণ্যের মধ্যে সবচেয়ে বেশি কমেছে গম। এ ছাড়া সয়াবিন বীজের আমদানিও কম। অন্যদিকে শিল্পের কাঁচামালে শুধু ক্লিংকারে এখনো প্রবৃদ্ধি রয়েছে। চলতি অর্থবছরে আট মাসে ক্লিংকার আমদানি হয় ১ কোটি ৩৮ লাখ টন। গত অর্থবছরের একই সময়ে ছিল ১ কোটি ৩৩ লাখ টন।

অর্থনীতির জন্য স্বস্তি নাকি অস্বস্তি

আমদানি ব্যয় কমার প্রভাবে সুবিধা বা অসুবিধা কী, জানতে চাইলে বেসরকারি গবেষণা প্রতিষ্ঠান সিপিডির বিশেষ ফেলো মোস্তাফিজুর রহমান প্রথম আলোকে বলেন, আমদানি কমায় ব্যালান্স অব পেমেন্টে (চলতি হিসাবে ভারসাম্য) সাময়িক স্বস্তি পাওয়া যাবে।

তবে আমদানি কমিয়ে রাখা মধ্যমেয়াদি কোনো সমাধান নয়। রপ্তানি ও প্রবাসী আয় বাড়াতেই হবে। আইএমএফের ঋণের ভালো ব্যবহার করতে হবে। অর্থনৈতিক ব্যবস্থা ভালো করে উচ্চ প্রবৃদ্ধিতে যেতে হবে। না হলে উৎপাদনের সঙ্গে সম্পর্কিত আমদানি ধারাবাহিকভাবে কমতে থাকলে বিনিয়োগ–কর্মসংস্থানে নেতিবাচক প্রভাব পড়বে।

সূত্রঃ প্রথম আলো