High volume of NPLs, rising cost of funds, falling deposits blamed

The bankers were, however, expecting the indicators to turn around a bit in the coming months thanks to the Bangladesh Bank (BB) sets a new interest rate mechanism based on the benchmark reference rate to be effective from next month.

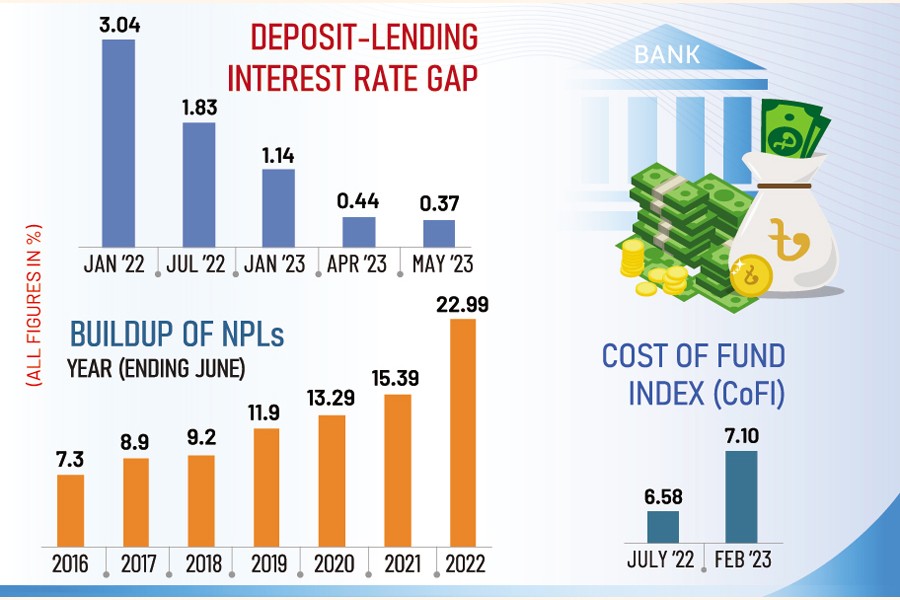

The spread, difference between weighted average rates of deposits and advances, was 0.44 per cent in the previous month and fell seven basis points in May, according to the BB statistics.

An official at the BB said the spread was 3.04 per cent even in January 2022 before starting falling and stood at 1.83 per cent in July 2022, followed by 1.14 per cent in January this year.

“The May figure is the lowest in the NBFIs’ history. It reflects how poor the health of the financial institutions here,” the official said, adding that other key indicators like NPLs and rising cost of funds and shrinking deposits also affected the sector badly.

The BB data shows the aggregate volume of NPLs of the NBFIs rose by over threefold in less than seven years. As a spillover effect, two major profitability-measuring indicators – return on asset (ROA) and return on equity (ROE) – keep falling alarmingly.

The volume of classified loans or leases was 7.3 per cent at the end of June 2016. Since then, the NPLs have been rising and jumped to 22.99 per cent in June 2022, when the NPLs stood at Tk 159.36 billion of the total loans amounting to Tk 693.32 billion.

The deposits stood at Tk 436.98 billion in January-March period of this year, which was slightly down from Tk 437.53 billion recorded in the previous quarter (October-December of 2022).

According to the Cost of Funds Index (CoFI) released by the central bank, the weighted average cost of funds in July 2022 was 6.58 per cent, and it continued to rise, reaching 7.10 per cent in February 2023.

Talking to the FE, Managing Director and CEO of IPDC Finance Mominul Islam said the spread in the NBFIs continues narrowing down as their income is shrinking, which is not at all a good sign for the industry.

He, however, expected that things will improve a bit in the coming months as the BB sets a new interest rate mechanism.

About the bad loans, he said the situation is deteriorating alarmingly mainly because of a massive-scale of irregularities by some of the 8-10 NBFIs in recent times.

Simultaneously, the impact of the pandemic coupled with the ongoing volatility in global macroeconomic situation after the war in Ukraine that put an extra pressure on the entire European business also contributed to some extent to the rise in bad loans.

“There are, however, many good NBFIs which maintain good corporate governance in delivering policy and process-driven lending mechanisms. Yes, the rising trend in the NPLs is a reality, but it’s mainly because of poor governance by some institutions,” he added.

Speaking on condition of anonymity, a top executive of an NBFI said that banks are now offering deposit rates as high as 8.0 per cent, which has caused many institutional depositors to withdraw their funds and move to banks for higher gains.

To remain in business under the current context, many NBFIs have started offering higher rates than the ceiling, raising their cost of funds, he said.

“There is a maximum lending cap of 11.0 per cent imposed by the BB from July 2022. So, the spread kept shrinking, which is a matter of serious concern for the sector,” the executive added.

Managing Director and CEO of Strategic Finance & Investments Limited (SFIL) Irteza Ahmed Khan said the growing NPLs have contributed to the rise in cost of funds and it ultimately impacted the profitability.

He said the NBFIs are operating their businesses in an uneven competition with the banks in the market where there was no deposit ceiling for banks.

But there is a deposit ceiling of 7.0 per cent and lending rate cap of 11 per cent for the banks. Though some of the NBFIs crossed it to get deposits and stay alive in the market, it badly affected the spread, he added.

Appreciating the BB’s latest interest rate mechanism based on SMART (Six-Months Moving Average Rate of Treasury Bill), he said it would help solve the problem.

Moreover, 1.0 per cent annual supervision charge has been introduced for the CMSMEs, consumer finance and auto loan products, which will now increase the overall yields onwards, he added.

Source: The Financial Express